With summer peaks pushing 45–50°C in cities such as Delhi, Jaipur, Nagpur, and Bhopal, affordable cooling has effectively become a basic utility for middle-class households across North and Central India. The numbers bear this out: according to IMARC Group, India’s air cooler market was valued at ₹126.1 billion (~USD 1.5 billion) in 2025 and is projected to nearly double to ₹235.1 billion by 2034, growing at a 6.81% CAGR over the forecast period.

In value-USD terms, a complementary estimate from ResearchAndMarkets and TechSci Research pegs the market at USD 148.65 million in 2024, expanding to USD 335.16 million by 2030 at a sharper 14.51% CAGR — a difference that reflects methodological scope rather than conflicting facts. Even on a year-on-year basis, the category posted ~7% value growth from ₹117.7 billion in 2024 to ₹126.1 billion in 2025, consistent with a market that responds sharply to both the annual heat calendar and rising Tier-2/3 purchasing power.

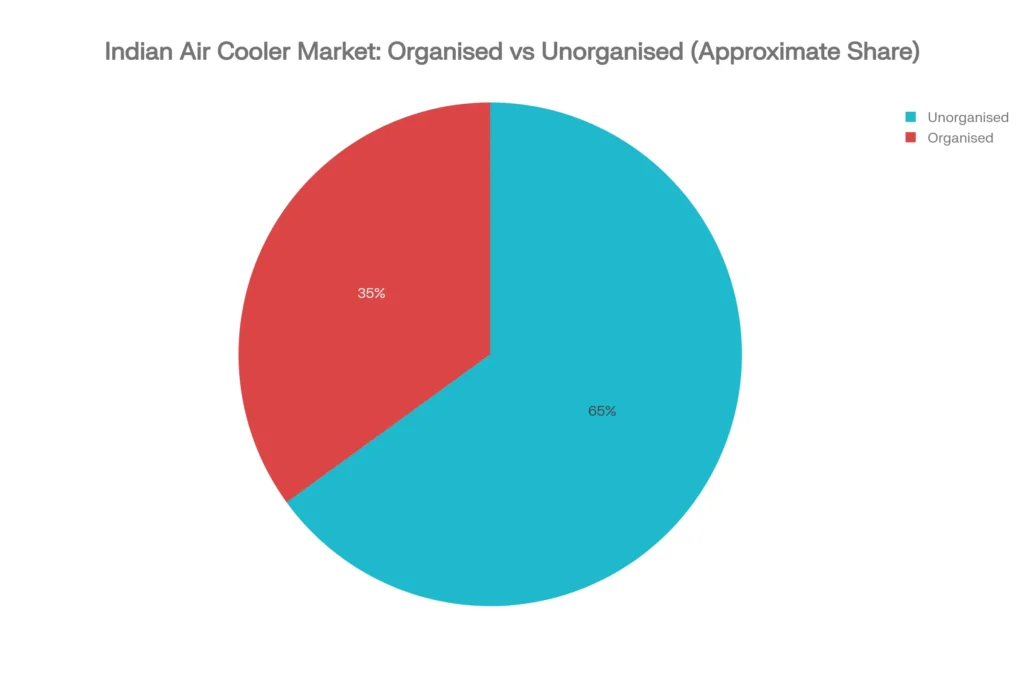

Driving this growth is a category led by a handful of large organized brands — Symphony, Bajaj Electricals, Havells, Voltas, and Crompton — but still characterized by the fact that unorganized “tin-body” coolers hold roughly 65–70% of market value and an even higher share of units shipped.

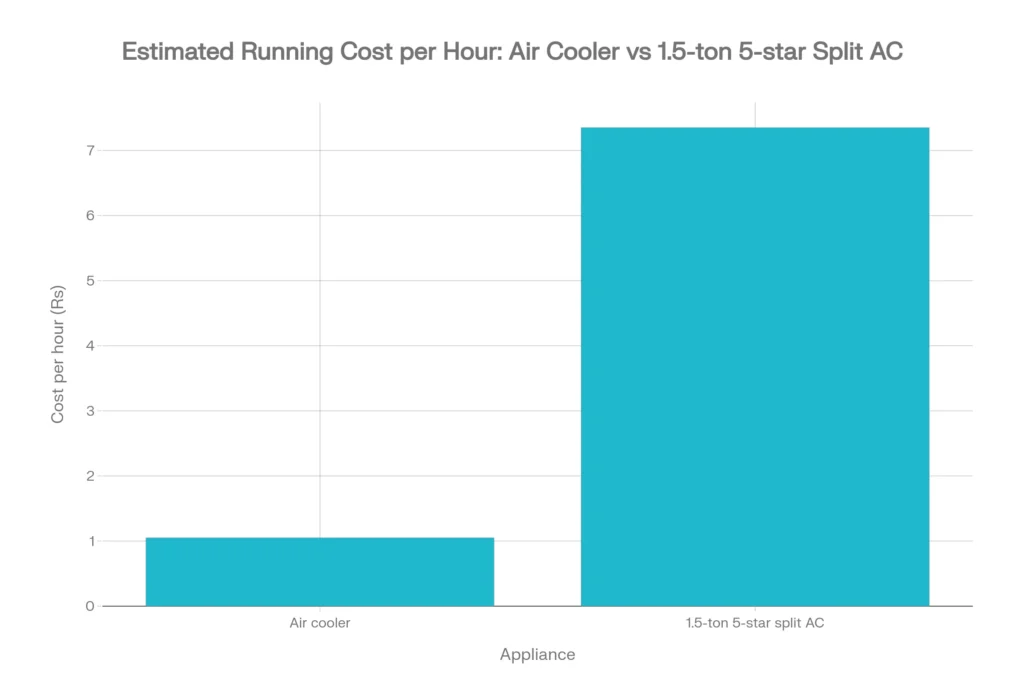

At the same time, rising electricity tariffs and a grid under increasing stress are nudging both consumers and policymakers towards low-energy evaporative air coolers over room ACs wherever climate conditions permit. As GadgetVeda has explored in this category deep-dive, the case for coolers in hot-dry zones is essentially a mathematical one: a typical desert air cooler draws 150–300 W versus the ~1,050 W average of a 1.5-ton 5-star inverter split AC, making the AC’s running cost roughly 7× higher per hour at standard Delhi-slab tariffs.

The India Cooling Action Plan (ICAP) and the Alliance for an Energy Efficient Economy (AEEE) both explicitly identify evaporative air coolers as a critical, low-GWP alternative to manage India’s cooling demand, which is expected to grow ~2.2× by 2027. The upshot: as incomes rise, heat seasons lengthen, and BEE star-rating frameworks for air coolers inch closer to reality, this is a market positioned for sustained double-digit value-level growth in the organized segment — with premiumization, BLDC motors, and basic smart features reshaping what consumers expect from a product that was once seen as purely utilitarian.

🛒 Ready to Shop by Budget? GadgetVeda Has You Covered.

The market data above tells you why the ₹5,000–₹10,000 band is where the best value lives. Our budget-specific guides tell you which exact model to pick within that band — reviewed, compared, and shortlisted for Indian summers.

🟢 Best Air Coolers Under ₹5,000— Top tin-body alternatives and best economy-branded picks

🔵 Best Air Coolers Under ₹6,000— Entry-level branded honeycomb coolers worth buying

🟡 Best Air Coolers Under ₹7,000— The sweet spot for performance vs price in 2026

🟠 Best Air Coolers Under ₹8,000— Mid-range desert and tower coolers with remote features

🔴 Best Air Coolers Under ₹10,000— BLDC motors, large tanks and smart features without breaking budget

Air Cooler Market in India [Quick Overview]

| Metric | Key Insights |

| India Air Cooler Market Size & Value (2025) | The all-India market — covering both organized brands and unorganized local players — stood at ₹126.1 billion (~USD 1.45 billion) in 2025. This includes desktops, towers, and personal coolers across residential and commercial use. The market has grown steadily from ₹117.7 billion in 2024, reflecting ~7% YoY value growth. |

| Implied 2026 Market Value | Applying IMARC’s reported 6.81% CAGR once to the 2025 base yields an estimated ₹134–135 billion for 2026 — firmly in the mid-₹130 billion band. This is a model-based extrapolation, not a directly published figure, and should be treated as a planning estimate. At ~₹87 per USD, this equates to approximately USD 1.5–1.6 billion. |

| Medium-Term Growth Outlook (2024–2031) | Most credible India-focused syndicated studies project a 7–11% CAGR in value terms through 2030–31. The spread reflects differing research scope: broader studies (domestic + commercial, all channels) show ~7%, while narrower or higher-ASP-segment studies cite up to ~14%. A 7–11% planning band is the most defensible working assumption for the overall market. |

| Organized vs Unorganized Split (2024–25) | Despite the growing visibility of branded players, unorganized “tin-body” coolers still hold ~65–70% of market value — and an even higher share of units shipped. The organized segment (branded, injection-molded plastic coolers) accounts for only ~30–35% of value but is growing faster. This conversion gap is the single biggest structural opportunity in the category. |

| Category Leader | Symphony Ltd commands approximately 50% value share within India’s organized air cooler segment, making it the dominant force in the branded tier by a wide margin. Its leadership spans residential desert coolers, personal coolers, and commercial/industrial units, supported by strong brand recall and a wide dealer network. |

| Top Organized Brands (Rest of Market) | The follower pack is fragmented but credible: Bajaj Electricals (wide general-trade reach, economy/standard focus), Havells India (premium design, BLDC motors), Voltas (leverages Tata/AC channel), Crompton and Kenstar (regionally strong, competitive online). Each operates in a single- to low-double-digit value share band within the organized segment. |

| Residential vs Commercial Mix | Residential demand accounts for ~80% of India’s air cooler market, with homeowners in hot-dry states driving the bulk of summer purchases. The commercial and industrial segment (~20%) — covering factories, warehouses, retail spaces, and offices — is the fastest-growing tail, as businesses seek affordable alternatives to expensive ducted AC systems. |

| Regional Demand Pattern | North and West India (Rajasthan, Gujarat, Delhi, UP, MP, parts of Maharashtra) dominate sales, benefiting from hot-dry summers where evaporative cooling works most effectively. Together, these regions account for the majority of both unit volumes and value. South and East India have lower penetration — higher humidity limits cooling efficiency — but are growing steadily as brands push tower coolers and awareness improves. |

| Pad Technology Trend | Honeycomb pads (cellulose, hexagonal structure) have become the standard in virtually all branded plastic-body coolers, offering better water retention, longer life, and lower maintenance vs older alternatives. Wood-wool (aspen) pads persist in low-cost tin-body and unorganized local coolers, where the upfront price is the primary driver. This pad-type divide closely mirrors the organized/unorganized split. |

| Running Cost: Air Cooler vs 1.5-Ton 5-Star Split AC | At Delhi-slab electricity tariffs (~₹7/kWh), a typical desert air cooler (~0.15 kW) costs roughly ₹1–1.50 per hour to run, versus ₹7–8 per hour for a 1.5-ton 5-star inverter split AC (~1.05 kW). That’s a ~7× gap in hourly running cost, translating to monthly electricity bill differences of ₹1,500–2,000+ for equivalent daily usage hours. In hot-dry climates, this math makes air coolers the rational default for cost-conscious households. |

Air Cooler Market in India: Market Size & Growth Outlook

Why Different Reports Give Different Numbers

If you have been researching this market and found wildly different figures across sources, you are not misreading them — the numbers genuinely differ because each research house draws its boundaries differently. Some include only domestic residential coolers; others bundle in commercial and industrial units. Some work in USD using spot FX; others use INR at trade prices. Tax treatment and channel definitions vary, too. None of these baselines is wrong — they just answer slightly different questions.

Here is what the three most widely-cited sources actually say:

IMARC / OpenPR (broadest India-level view): Market at ₹117.7 billion in 2024, growing to ₹126.1 billion in 2025, and forecast to reach ₹229.47–235.1 billion by 2033–34 — implying a ~6.8–7.1% CAGR over the coming decade.

The Insight Partners / Business Market Insights (domestic + commercial scope): Market at USD 549.53 million in 2024, reaching USD 1,134 million by 2031 at a 10.9% CAGR — a faster rate that reflects the faster-growing commercial cooling sub-segment pulling the average up.

TechSci / GII Research (narrower channel/product scope): Market at USD 148.65 million in 2024, expanding to USD 335.16 million by 2030 at a sharper 14.51% CAGR — the highest rate, but for a narrower slice of the overall market.

Where Does That Leave 2026?

No major syndicated study publishes a standalone 2026 India INR figure, so we derive one transparently. IMARC reports ₹126.1 billion for 2025 and a 6.81% CAGR from 2026–2034. Applying that growth rate once gives an estimated ₹134–135 billion for 2026 — call it the mid-₹130 billion band. At an average FX of ~₹87 per USD, that converts to approximately USD 1.5–1.6 billion. Treat this as a planning estimate, not a reported figure.

For strategic purposes, the 7–11% value CAGR band is the most defensible working range for the overall India air cooler market through 2030, with the lower end representing the broad market and the upper end reflecting the faster-moving organized and commercial segments.

What Symphony’s Brokers Say About the Domestic TAM

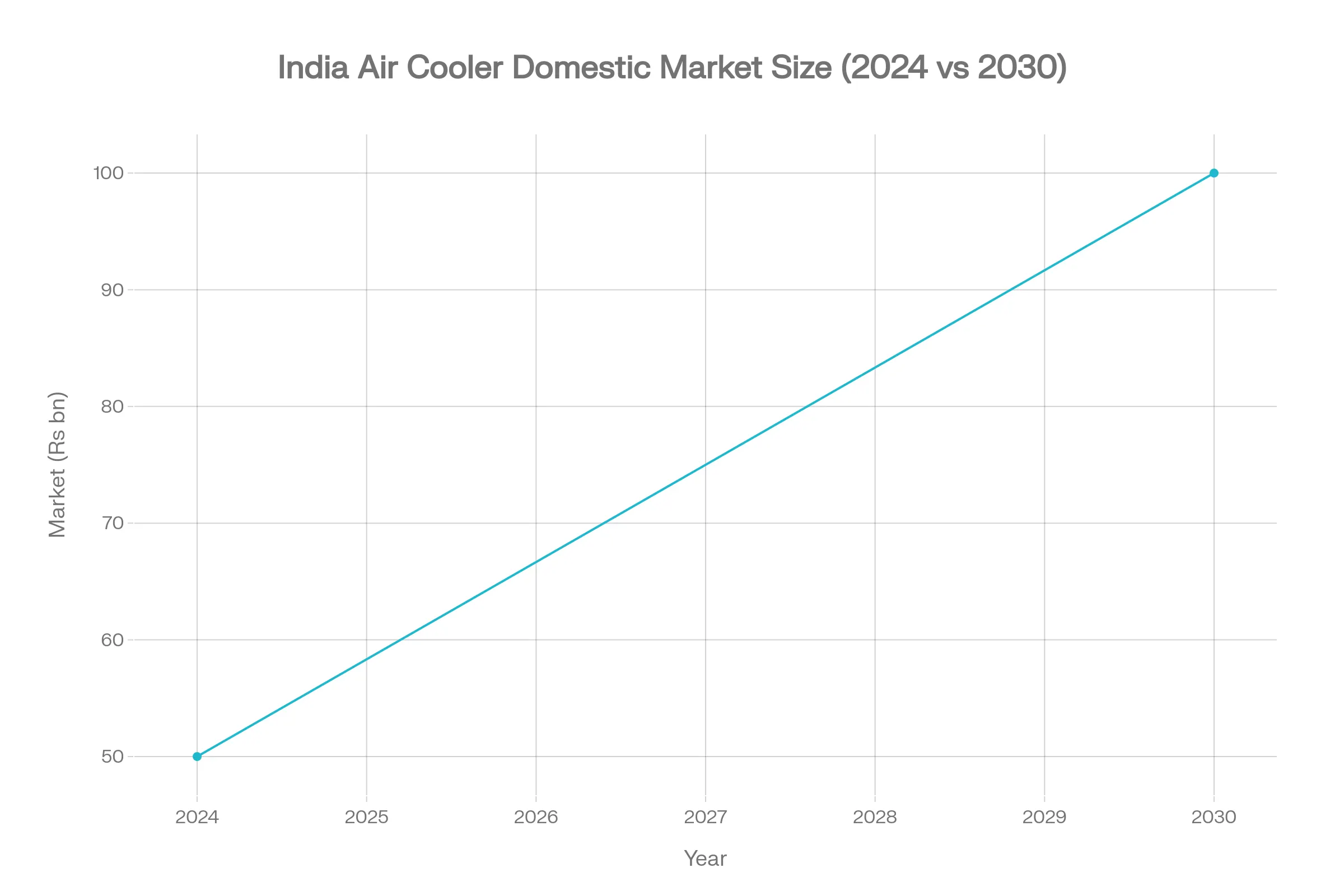

Beyond syndicated research, the most grounded domestic view comes from SMIFS’s 2025 initiating coverage note on Symphony, which draws directly on management commentary. It pegs the Indian domestic air cooler market size at ~₹50 billion in CY2024, with the organized segment accounting for ~35% of that. Crucially, the same report expects that domestic TAM to reach ~₹100 billion within 5–7 years, implying a ~12.2% CAGR over FY24–30 — faster than the broader syndicated range, but consistent with it once you strip out export revenues and commercial-channel overlaps.

Market Structure: Organized Brands vs Local Tin-Body Players

| Dimension | Organized Players (Symphony, Bajaj, Havells, Voltas, Crompton, etc.) | Unorganized / Local Tin-Body Players |

| Approx. Value Share | ~30–35% of the total Indian air cooler market value. A minority by value today, but this share is growing steadily as branded coolers penetrate Tier-2/3 cities and consumer awareness around efficiency and durability rises. | ~65–70% of market value — and an even higher share of units shipped. The unorganized segment’s dominance is especially pronounced in desert coolers, where local fabricators can price aggressively by avoiding R&D, warranty, and distribution costs. |

| Typical Product Types | Injection-molded plastic-body coolers — spanning personal coolers (10–20L), room coolers (30–50L), tower coolers, and large-format commercial/industrial units. Products carry formal warranties, standardized specs, and national service support. | Sheet-metal “tin-body” desert coolers — typically fabricated locally in small workshops, available in standard desert-cooler sizes. Build quality and efficiency vary widely. No formal warranty or after-sales infrastructure in most cases. |

| Cooling Pad Technology | Honeycomb pads are now standard across virtually all mainstream branded SKUs from Symphony, Bajaj, Crompton, Orient, and others. Honeycomb’s superior water retention, longer lifespan, and lower maintenance make it the natural fit for branded, warranty-backed products. | Wood-wool (aspen) pads remain the default in most organized tin-body coolers, valued for low cost and high water absorption. Honeycomb pads are slowly appearing in higher-priced local builds, but replacement availability and quality consistency remain patchy. |

| Price Positioning | Core sweet spot: ₹5,000–₹12,000+, covering the Standard and Premium segments. Select brands (Bajaj, Crompton, Kenstar) offer entry-level plastic coolers below ₹5,000, but organized brands generally avoid competing at the very bottom on price alone. | Dominant in the sub-₹5,000 Economy band — including the cheapest desert and room coolers in the market. Low-mid desert cooler formats (₹3,000–₹5,500) are the core strength, where material and labor cost advantages over brands are largest. |

| Motor Technology | Increasingly featuring BLDC (Brushless DC) motors in mid-to-premium SKUs, offering up to 60% motor energy savings vs conventional induction motors and meaningfully lower noise levels. Conventional induction motors are still used in economy-end branded models. | Conventional induction motors are standard across virtually all local fabricator units — with no energy-efficiency rating, no BLDC adoption, and no BEE compliance pathway in sight for most players. |

| Sales & Distribution Channels | Modern trade, large-format appliance retailers (Reliance Digital, Croma), brand-owned stores, national e-commerce platforms (Amazon, Flipkart), and a structured dealer/distributor network. Brands increasingly use digital channels for consumer outreach and after-sales. | Local fabricators, unorganized hardware stores, semi-organized regional distributors, and small offline shops. Heavily concentrated in the North and West India heat-belt towns. Little to no e-commerce presence; purchase driven almost entirely by proximity and price. |

| After-Sales & Warranty | 1–2 year product warranties with national service networks, spare parts availability (especially for pads and pumps), and brand helplines. This total-cost-of-ownership advantage is increasingly important to urban and semi-urban buyers. | No formal warranty in most cases. Repairs depend on the local fabricator or an informal technician. Pad and pump replacements are cheap but quality-inconsistent. Total cost of ownership over 3–5 years can exceed that of a branded cooler once repairs are factored in. |

| Growth Direction | Gaining share gradually — driven by rising incomes, growing awareness of energy efficiency, BEE star-rating discussion,s and e-commerce penetration into Tier-2/3 markets. The organized segment is the primary beneficiary of the category’s premiumization cycle. | Losing value share slowly, but is still dominant in volume. Local players benefit from deep regional relationships, cash-based trade, and near-zero overhead. Their share is unlikely to collapse quickly — but the structural drift is clearly away from tin-body and toward branded plastic. |

The Branded Segment Is Growing — But Still the Minority

Here is a fact that surprises most people encountering this category for the first time: the large, well-marketed brands you see on e-commerce platforms represent only about 30–35% of India’s air cooler market by value. The remaining 65–70% — and an even higher share of units sold — comes from local, unorganized manufacturers, primarily sheet-metal “tin-body” desert cooler fabricators concentrated in North and Central India.

This is not a legacy anomaly about to vanish. AEEE’s demand analysis for cooling in India notes the organized-unorganized value split at approximately 30:70, while broker research on Symphony consistently places the organized segment at ~35% of the ₹50 billion domestic market — both reinforcing the same structural picture. The gap is especially pronounced in desert coolers, where local fabricators can undercut branded players significantly by skipping R&D, warranty infrastructure, and national distribution costs.

The good news for branded players: the direction of travel is clearly towards organization. As Tier-2 and Tier-3 disposable incomes rise and consumers pay more attention to energy bills and product durability, the economic case for a branded cooler gets stronger. But the conversion opportunity is enormous — roughly two-thirds of the market is still up for grabs.

Brand Leaderboard: Who Owns the Organized Market

Symphony: The Category Defines the Brand, and Vice Versa

Ask most Indian consumers to name an air cooler brand, and there is a high probability the answer is Symphony. That recall is earned: according to Symphony’s own annual reports and independent equity research from Sharekhan, SMIFS, and others, the company commands approximately 50% value share within India’s organized air cooler segment — a dominance that has held up across multiple cycles.

Symphony’s portfolio spans personal coolers, residential desert and room coolers, and large-format commercial units, giving it coverage across nearly every organized sub-segment. Its FY22-23 Annual Report explicitly describes it as “India’s biggest air cooler brand”, and broker notes consistently benchmark the competition relative to Symphony’s half-share, which tells you everything about how far ahead it sits.

The Follower Pack: Fragmented but Competing Hard

Behind Symphony sits a credible but fragmented group of challengers. No public Indian data source prints a clean brand-by-brand share table for air coolers, so the responsible view is directional ranges rather than point estimates:

Bajaj Electricals is arguably the largest organized follower, with wide general-trade distribution and strong presence in the economy and standard plastic desert/personal coolers.

Havells India focuses on the premium design and efficiency angle, with BLDC motor-led models that appeal to urban, energy-cost-aware buyers.

Voltas uses its established AC dealer network and Tata brand equity to cross-sell coolers in hot-dry West and North India, with a credible but smaller footprint.

Crompton and Kenstar hold regionally strong positions, with competitive online-first SKUs and growing brand visibility in the mid-range.

Each of these brands operates in a single- to low-double-digit value share band within the organized segment — meaningful, but not close to Symphony’s dominance.

Regional Insights: Where India Buys Its Coolers

North and West India Are the Engine

The geography of air cooler demand in India is not subtle. North and West India — covering Rajasthan, Gujarat, Delhi, UP, MP, Haryana, Punjab, and parts of Maharashtra — generate the lion’s share of both volumes and value, driven by summers that routinely exceed 40–45°C with relatively low humidity. This combination is exactly where evaporative cooling works best: high heat, dry air, and adequate ventilation let a cooler bring room temperatures down by 8–12°C at a fraction of AC running cost.

The Insight Partners’ India domestic and commercial air cooler report specifically highlights March–May 2024 data showing cities like Guna and Sagar (MP) and Akola (Maharashtra) recording 41.6–42.6°C and above, with multiple districts in Gujarat and Rajasthan crossing 45°C — events that translate almost directly into sales spikes at local dealers and on e-commerce platforms. The India Cooling Action Plan further identifies these hot-dry zones as priority geographies for promoting energy-efficient cooling, reinforcing the structural long-term case for air coolers in this belt.

South and East India: Smaller, But Worth Watching

In the more humid states of South India — Tamil Nadu, Kerala, coastal Karnataka, and Andhra Pradesh — and across East India, air cooler penetration is structurally lower. Higher ambient humidity limits evaporative cooling’s effectiveness, making ACs a stronger proposition despite the higher cost.

That said, brands are not ignoring these markets. Tower coolers with higher airflow and designs that work in moderate-humidity conditions are being pushed into southern urban markets. More importantly, South and East are expected to grow faster off a lower base, especially in semi-urban areas where AC ownership costs remain a stretch. The region is best understood as a medium-term opportunity rather than a core market today.

Price Segment Dynamics: Economy, Standard, and Premium

You will not find a published, precise “% of market by price band” figure in any credible India air cooler report — and any source claiming to give you one to two decimal places should be treated skeptically. What retail data, brand catalogs, and buying-guide search trends do tell us, clearly, is how each segment behaves:

Economy (Below ₹5,000): This is where unorganized tin-body desert coolers live, alongside the cheapest personal coolers from value-brand sub-lines. Demand here is enormous in volume — “best air cooler under ₹5,000” is one of the highest-traffic cooler search queries in India every summer — but margins are thin, and the customer is almost entirely price-driven. Organized brands have limited presence here and generally do not want to compete on these terms.

Standard (₹5,000–₹9,000): This is the primary battlefield for organized brands and almost certainly the largest segment by value. Mainstream branded desert and room coolers — typically with 30–50L tanks, honeycomb pads, basic remote options, and plastic injection-molded bodies — cluster here. Symphony, Bajaj, Crompton, and Kenstar all have their highest-volume SKUs in this band.

Premium (Above ₹9,000): The fastest-growing segment by value-growth rate, even if it remains the smallest by volume. BLDC motor models, large-format tower coolers, IoT-enabled smart coolers, and design-forward builds all live above ₹10,000–₹12,000. Urban buyers trading up for lower noise, smarter controls, and better energy efficiency are driving this tier, and brands are investing accordingly.

Technology Adoption: Pads, Motors, and Smart Features

Honeycomb vs Wood-Wool: The Pad Divide Is Also the Market Divide

The type of cooling pad inside a cooler tells you almost everything about where it sits in the market. Honeycomb pads — made from cellulose in a hexagonal structure — deliver better water retention, higher cooling surface area, longer usable life, and easier cleaning than their older counterparts. They cost more to produce, which is why virtually every branded plastic-body cooler from Symphony, Bajaj, Crompton, Orient, and others now ships with honeycomb as standard.

Wood-wool (aspen) pads, by contrast, are cheaper and absorb water well, but degrade faster and need more frequent replacement, which makes them well-suited to the price-first logic of the unorganized tin-body segment, where the buyer’s primary filter is upfront cost, not total cost of ownership. The pad-type divide, in other words, very closely mirrors the organized-versus-unorganized market split: honeycomb dominates branded shipments, wood-wool dominates the local fabricator market.

BLDC Motors: The Efficiency Upgrade That’s Quietly Going Mainstream

Brushless DC (BLDC) motors are to air coolers what inverter compressors were to ACs a decade ago — an efficiency upgrade that starts in the premium tier and gradually filters down. Brands including Kenstar and Symphony highlight that BLDC motors can reduce motor electricity consumption by up to 60% versus conventional induction motors, while also running significantly quieter.

Right now, BLDC adoption is concentrated in mid-to-premium branded models — typically above ₹8,000–₹10,000. But with the Bureau of Energy Efficiency (BEE) reportedly exploring a star-rating framework for air coolers, the market dynamic could shift meaningfully. Once efficiency ratings become a visible purchase filter — as they did for ACs, refrigerators, and fans — brands that have already standardized BLDC motors will have a structural marketing advantage, and buyers will have a cleaner way to compare running costs before purchase.

IoT and Smart Coolers: Real Trend, Still Early Days

Bajaj’s Cool.iNXT was among the earliest widely marketed Wi-Fi-enabled, app-controlled air coolers in India — operable via smartphone, IR remote, and on-panel controls. Today, most leading brands offer at least one or two SKUs with remote control and auto-louver features, though full app-based IoT control remains concentrated in the >₹10,000 premium band.

Market outlook commentary from multiple analysts forecasts wider IoT cooler adoption by 2028, especially as urban household Wi-Fi penetration deepens and consumers grow more comfortable with smart-home devices. In volume terms, smart and IoT models are almost certainly below 5% of total units today, but their growth rate within the organized segment is meaningfully faster than the base market. Think of it as the same trajectory that smart TVs followed: niche today, expected standard within five years.

Energy Efficiency: Air Coolers vs 5-Star Split ACs

The Power Draw Gap Is Larger Than Most People Realize

The energy difference between an air cooler and a split AC is not marginal — it is structural and significant. A typical desert air cooler runs on 150–300 W; tower and personal coolers often draw even less, in the 100–200 W range. A 1.5-ton 5-star inverter split AC, widely considered the most energy-efficient mainstream AC in India, still averages around 1.0–1.1 kW (1,000–1,100 W) under real-world conditions.

At a Delhi-slab electricity tariff of ~₹7 per kWh, the maths works out like this:

Air cooler (~0.15 kW average): ≈ ₹1.05 per hour, or roughly ₹250–800 per month depending on hours of daily use.

1.5-ton 5-star inverter split AC (~1.05 kW average): ≈ ₹7.35 per hour, translating to monthly bills of ₹1,700–₹2,500+ at similar usage hours.

That is a ~7× gap in hourly running cost, and it widens further in states with higher per-unit tariffs or where summer usage extends beyond eight hours a day. Over a three-to-five-year ownership window, the cumulative electricity saving from choosing a cooler over an AC in an eligible climate can comfortably offset the entire purchase price of the cooler — often multiple times over.

Why This Matters Beyond the Household Budget

The energy case for air coolers extends beyond individual electricity bills. The India Cooling Action Plan (ICAP) and the Alliance for an Energy Efficient Economy (AEEE) both explicitly identify evaporative air coolers as a priority low-GWP, low-energy tool for managing India’s surging cooling demand. Unlike split ACs, air coolers do not use high-GWP refrigerants — they cool via water evaporation, with near-zero direct emissions.

With India’s cooling energy consumption projected to grow ~2.2× by 2027, even a partial substitution of AC demand by air coolers in hot-dry zones — where the technology actually works — could meaningfully reduce peak grid load and carbon intensity of cooling. This is exactly why policymakers and urban planners are paying closer attention to the category. For consumers in Delhi, Rajasthan, Gujarat, and MP specifically, the air cooler is not a compromise — it is the rational, data-backed choice.

Air Cooler Market in India [2026 Trendlines]

Growth Is Real, but Volatile Year to Year

The 7–11% value CAGR consensus across major India air cooler reports is directionally reliable, but it masks significant year-to-year volatility. Annual volumes are highly weather-sensitive: a cooler summer in North India — as seen occasionally when pre-monsoon rains arrive early — can dent unit sales even as the long-run trajectory remains firmly upward. Brands and investors in this space have to plan for multi-year averages, not single-season outcomes.

Premiumization and Formalization Are the Twin Growth Engines

Within the organized segment, the clearest directional signal is premiumization: growth is skewed towards honeycomb-pad, BLDC-motor, tower-form-factor, and smart-feature models priced above ₹9,000–₹10,000, as urban buyers trade up for lower noise, better aesthetics,s and lower running costs. Simultaneously, the formalization of the conversion of unorganized buyers to branded products is expanding the organized segment’s share gradually from its current ~30–35% base.

Both forces are structural and mutually reinforcing: as more consumers buy branded coolers, category awareness around efficiency, pad quality, and after-sales service rises, making the next trade-up cycle easier.

Policy and Efficiency Norms Will Reshape the Category

BEE’s ongoing exploration of a star-rating framework for air coolers — combined with the broader cooling efficiency push under ICAP — means efficiency is shifting from a marketing claim to a regulated, verifiable attribute. Brands that have invested in BLDC motors, honeycomb pad standardization, and measurable efficiency metrics are best positioned when ratings become a mainstream purchase filter. Those still selling primarily on tank size and price will face growing pressure from both policy and better-informed consumers.

How Consumers Actually Shop This Category

Search volume data and retail content patterns reveal a consistent behavior: Indian consumers shop air coolers primarily within budget brackets. “Best air cooler under ₹5,000” and “best air cooler under ₹10,000” dominate search intent, with buyers then filtering by tank size, pad type, and features within their chosen band.

Online platforms have become the primary discovery channel — especially for urban buyers researching features and reading reviews — but offline dealers and local shops remain critical for fulfillment, particularly for desert coolers in North and West India, where product sizes and last-mile logistics make online delivery less seamless.

Finally, while residential demand (~80% of the market) will remain the dominant driver, the commercial and industrial segment — factories, warehouses, large retail spaces — is emerging as a fast-growing secondary market as facility managers price out the operating-cost difference between air coolers and ducted ACs at scale.

Conclusion

India’s air cooler market in 2026 is not a stagnant or commoditized category — it is a ₹130–140 billion growth story built on structural tailwinds: record-breaking summers, a grid that cannot yet support blanket AC adoption, and a middle class that is rapidly trading up from tin-body units to branded, energy-efficient models. The organized segment, though still only about a third of market value, is growing faster than the whole, led by Symphony’s near-unassailable 50% value share in the branded tier and a credible challenger pack in Bajaj, Havells, Crompton, and Voltas.

The data converges on a few clear verdicts. First, evaporative cooling remains the most cost-rational choice for households across North, West, and Central India — a cooler costs roughly one-seventh to one-eighth as much to run per hour as a 1.5-ton 5-star split AC, and that gap only widens as summer tariff slabs kick in.

Second, the sweet spot for buyers sits firmly in the ₹5,000–₹9,000 Standard band: branded honeycomb pads, increasingly standard BLDC motors, and better after-sales networks make this tier a rational step up from cheap tin-body alternatives, without stretching into the still-niche IoT premium. Third, the next 5 years will be defined not by explosive new technology but by conversion — pulling India’s 65–70% unorganised volume base towards branded, efficient, increasingly smart coolers as incomes rise and efficiency norms tighten.

For consumers, the story is simple: if you live in a hot-dry zone and haven’t upgraded from a local tin-body cooler, you are almost certainly paying more over three summers than a mid-range branded cooler would have cost you in the first place. The numbers are on the side of the upgrade.

![12 Best Air Conditioners Under ₹45,000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Best-Air-Conditioners-Under-₹45000-in-India-150x150.webp)

![Best Double Door Refrigerators Under 35000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/best-refrigerators-under-35000-in-India-150x150.webp)

![10 Common Washing Machine Problems & Solutions [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Common-Washing-Machine-Problems-Solutions-150x150.webp)

![10 Best Laptops Under ₹55,000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Best-Laptops-Under-₹55000-in-India-150x150.webp)

![12 Best Air Conditioners Under ₹45,000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Best-Air-Conditioners-Under-₹45000-in-India-300x167.webp)

![Best Double Door Refrigerators Under 35000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/best-refrigerators-under-35000-in-India-300x167.webp)

![10 Common Washing Machine Problems & Solutions [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Common-Washing-Machine-Problems-Solutions-300x167.webp)

![10 Best Laptops Under ₹55,000 in India [2026]](https://gadgetveda.com/wp-content/uploads/2026/07/Best-Laptops-Under-₹55000-in-India-300x158.webp)